Automotive parts company LKQ (NASDAQ:LKQ) missed Wall Street’s revenue expectations in Q1 CY2025, with sales falling 6.5% year on year to $3.46 billion. Its non-GAAP profit of $0.79 per share was 1.5% above analysts’ consensus estimates.

Is now the time to buy LKQ? Find out in our full research report .

LKQ (LKQ) Q1 CY2025 Highlights:

ANTIOCH, Tenn., April 24, 2025 (GLOBE NEWSWIRE) -- LKQ Corporation (Nasdaq: LKQ) today reported first quarter 2025 financial results. “We are pleased with our first-quarter performance and are driven to sustain this momentum as we advance our operational excellence initiatives and generate long-term value despite market uncertainties. By embracing these initiatives, even with lower demand, the team's unwavering focus on optimizing the Company’s cost structure is reflected in our year-over-year EBITDA percentage growth” stated Justin Jude, President and Chief Executive Officer.

Company Overview

A global distributor of vehicle parts and accessories, LKQ (NASDAQ:LKQ) offers its customers a comprehensive selection of high-quality, affordably priced automobile products.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, LKQ’s sales grew at a weak 2.6% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. LKQ’s annualized revenue growth of 5% over the last two years is above its five-year trend, but we were still disappointed by the results.

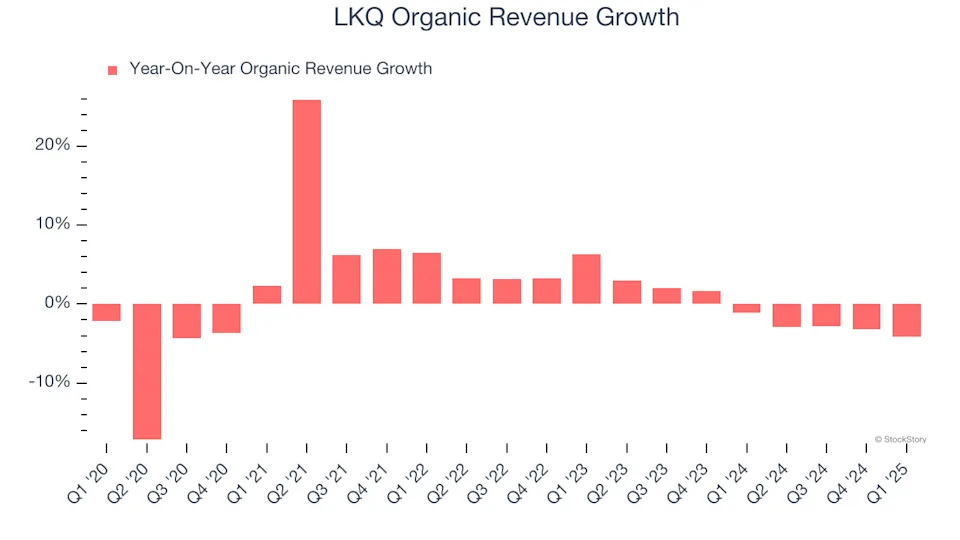

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, LKQ’s organic revenue was flat. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, LKQ missed Wall Street’s estimates and reported a rather uninspiring 6.5% year-on-year revenue decline, generating $3.46 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

Operating Margin

LKQ’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 8.7% over the last two years. This profitability was mediocre for a consumer discretionary business and caused by its suboptimal cost structure.

In Q1, LKQ generated an operating profit margin of 8.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

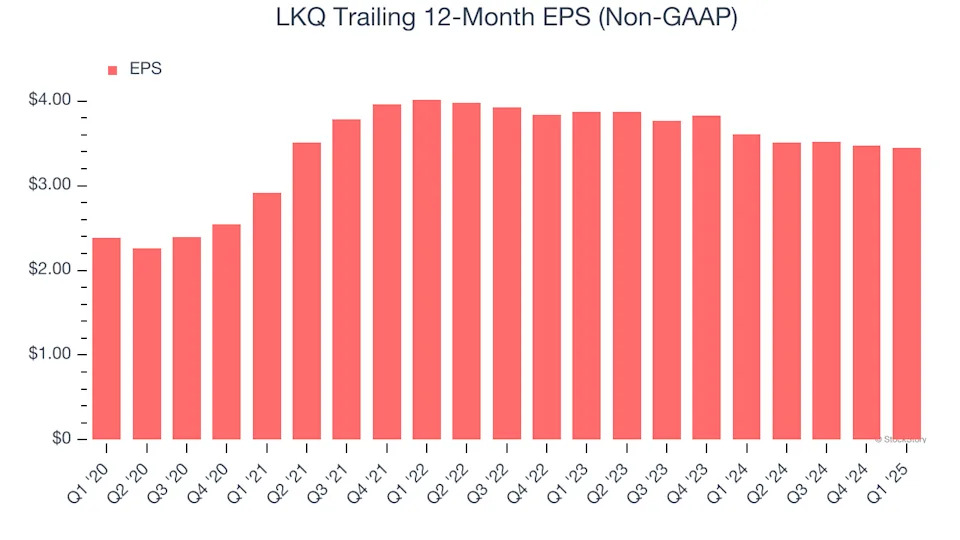

LKQ’s EPS grew at an unimpressive 7.6% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t expand.

In Q1, LKQ reported EPS at $0.79, down from $0.82 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 1.5%. Over the next 12 months, Wall Street expects LKQ’s full-year EPS of $3.44 to grow 6.5%.

Key Takeaways from LKQ’s Q1 Results

We struggled to find many positives in these results. Its full-year EBITDA guidance missed significantly and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 5% to $40.02 immediately following the results.

LKQ underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free .