(Bloomberg) — Traders are increasingly betting that the Federal Reserve will cut interest rates only once this year amid signs of resilient growth and sticky inflation.

Wednesday brings US consumer-price data for May, which is forecast to show a pickup that may reinforce the Fed’s wait-and-see stance toward further easing as it assesses the impact of tariffs. The central bank is widely projected to hold rates steady next week, and futures and options tracking expectations for its policy path show traders are moving to unwind the rate-cut premium built into the months ahead.

Swaps traders now see about 0.45 percentage point of easing by year-end, the smallest degree of reductions they’ve priced in since before President Donald Trump rolled out steep tariffs in early April. The announcement roiled markets and at one point in the following weeks led traders to wager on as much as a full point of Fed cuts by the end of 2025.

Stronger-than-forecast jobs data for May helped spur traders to exit easing bets. But the rate outlook had already been shifting in that direction, in part on hints of cooling trade tensions, which diminished further with talks between the US and China in London this week.

In options linked to the Secured Overnight Financing Rate, or SOFR, there has been a pickup in hedging activity targeting around just one or even no Fed policy moves this year.

Monday’s trading included heavy demand for hawkish protection via a range of structures looking to the end of this year and into early 2026, which Tuesday’s open interest showed were new positions. These types of wagers rise in value as rate-cut pricing fades from the futures underlying the options.

Here’s a rundown of the latest positioning indicators across the rates market:

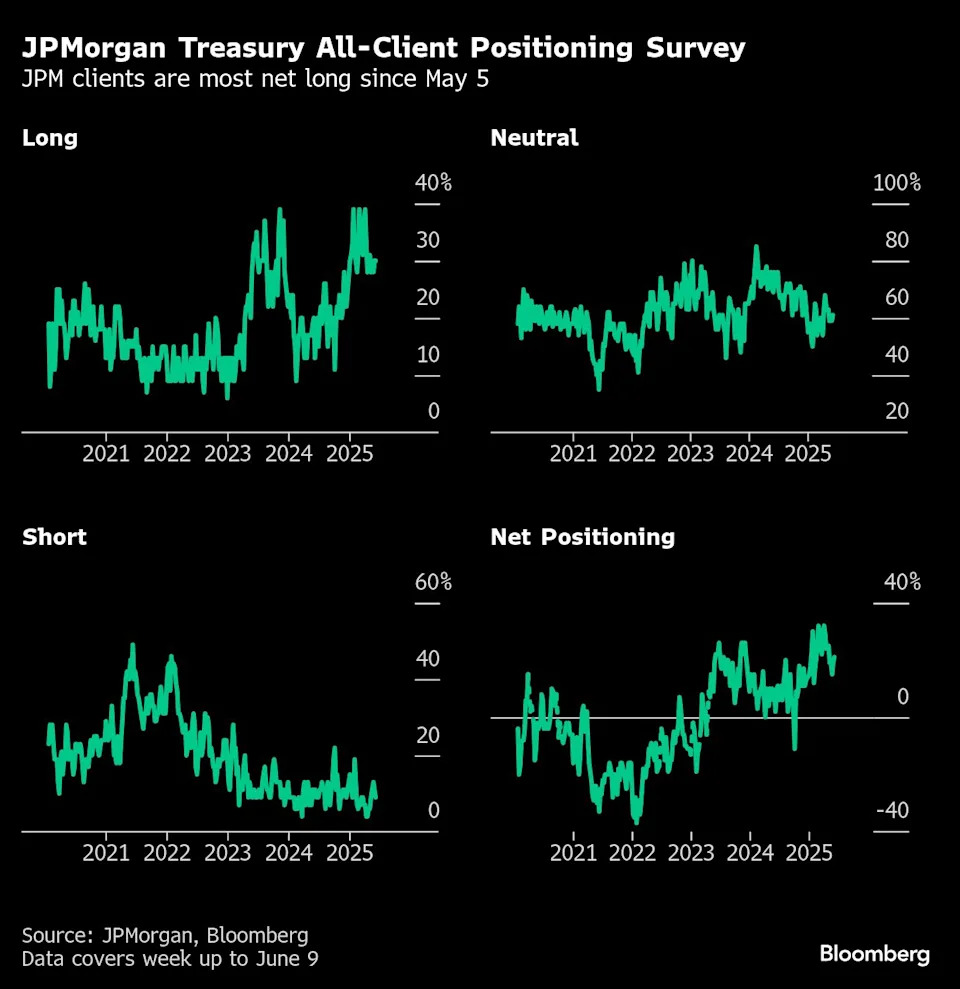

JPMorgan Treasury Client Survey

In the cash market, Tuesday’s JPMorgan Chase & Co. Treasury client survey showed investors’ net long position rose to the biggest since May 5. In the week to June 9, investors’ shorts fell 2 percentage points and neutrals rose by that amount.

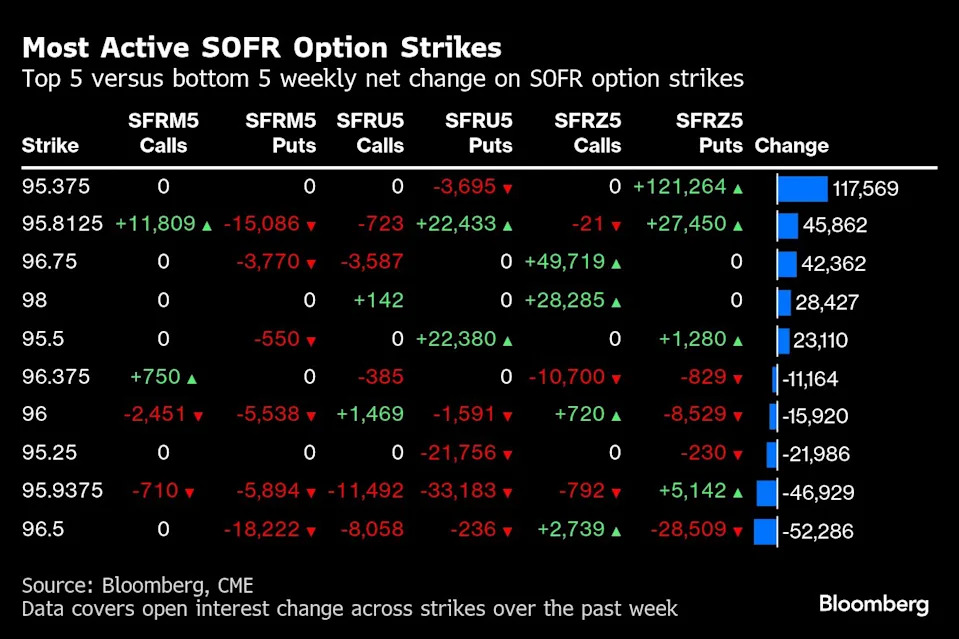

Most Active SOFR Options

For SOFR options across Jun25, Sep25 and Dec25 options there was a heavy amount of new risk in the Dec25 95.375 puts following big buying in the SFRZ5 95.625/95.375 put spread, targeting no Fed cuts this year. There was also a lot of activity seen in the 95.8125 strike over the past week due to more hawkish hedging via a buyer of the SFRZ5 95.8125/95.6875/95.5625 put fly. The past week has also seen new positioning in the 96.75 strike following trades such as SFRZ5 96.25/96.75 1x2 call spread which has been recently bought.

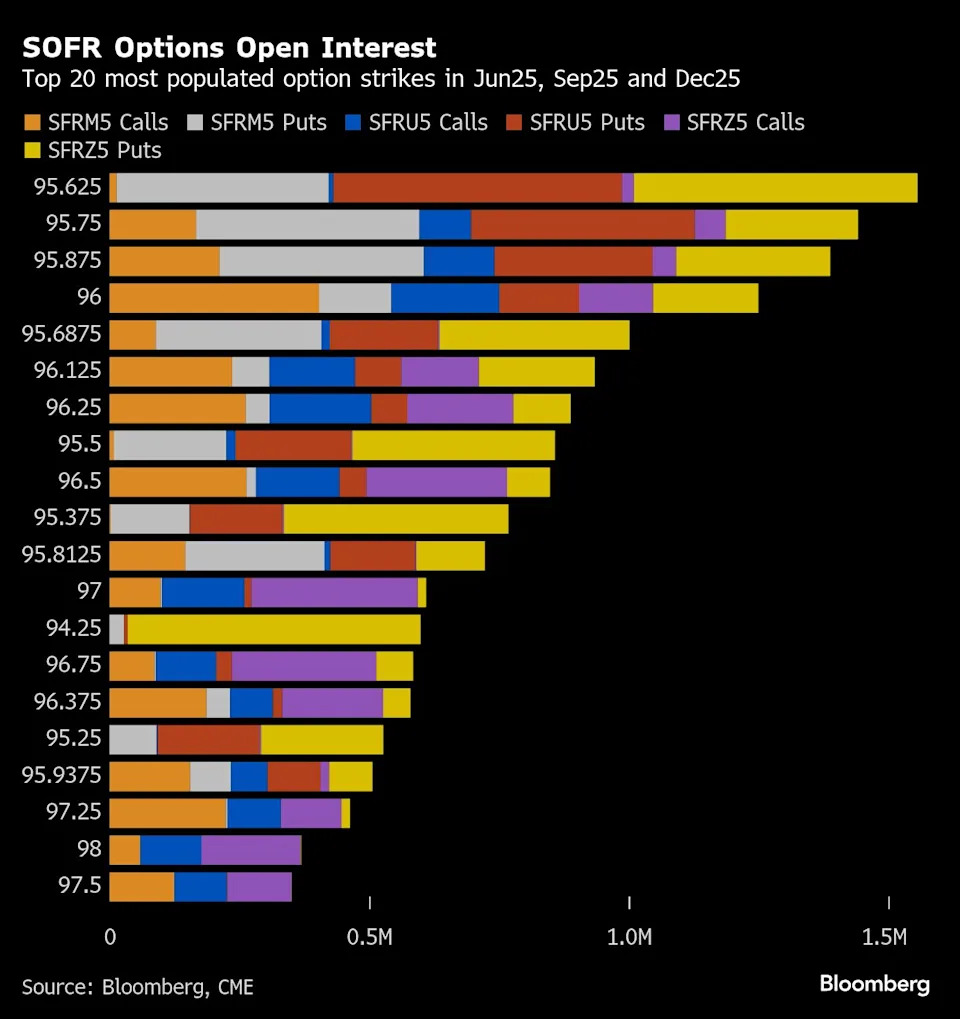

SOFR Options Heatmap

The 95.625 strike remains the most-populated position in tenors across Jun25, Sep25 and Dec25 options, mostly due to large positioning around the Jun25 puts via the SFRM5 95.75/95.625 put spread, which has recently traded. Recent flows in SOFR options since Friday’s payrolls have included hawkish hedges as rate-cut premium continues to fade from the underlying futures contracts over the next 18 months. The downside structures have been targeting puts in the Dec25 and Mar26 tenors.

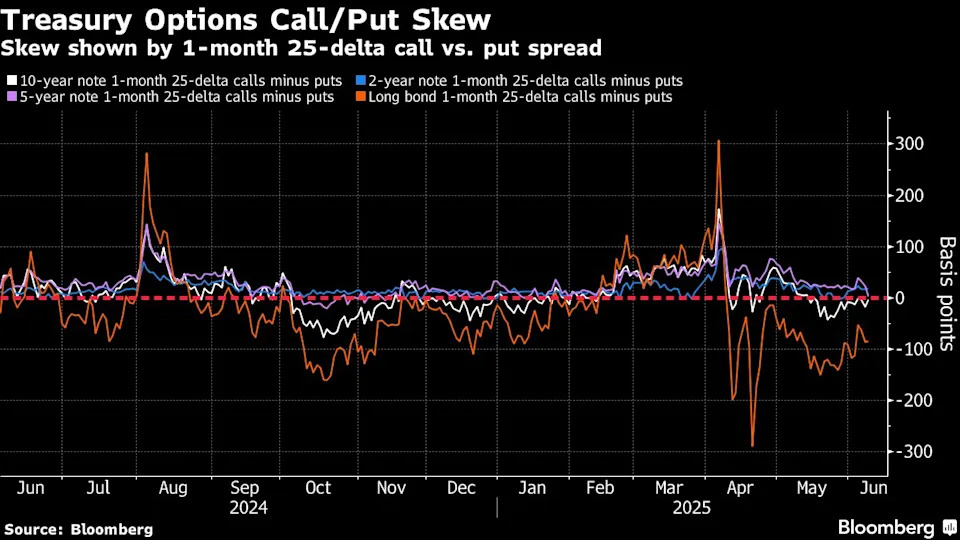

Treasury Options Skew

Traders are continuing to pay increasing premiums to hedge a selloff in the long-bond contracts on both an outright basis and relative to the front and belly of the curve. Long-bond skew, however, has been drifting closer to neutral over the past week as 30-year yields have run into resistance around the 5% level. The skew on the 10-year tenor trades around neutral, with some indication that CTA accounts may be entering fresh long positions in the TY contract.

CFTC Futures Positioning

Asset managers aggressively added to net duration long in Treasury futures across the strip in the week ended June 3, CFTC data show. This follows three weeks of de-leveraging via the liquidation of new long positions. The duration increase amounted to approximately 452,000 10-year note futures equivalents, the biggest weekly shift since April last year. Most of the net-long addition was in the ultra 10-year note futures, where around $11.3m/DV01 of net long risk was added.